- What is the MoneyLion App?

- Best 25+ Cash Advance Apps Like MoneyLion

- Why Do Cash Advance Apps Work?

- Payday Loan Apps vs. MoneyLion App

- Top 7 Key Features to Look for in a Cash Advance App Like MoneyLion

- How Much does It Cost to Develop a Cash Advance App?

- Conclusion

- Frequently Asked Questions About Cash Advance Apps

The fintech industry is undergoing rapid transformation, with the global market projected to surpass $300 billion, fueled by the rising demand for fast, accessible Digital financial services. Among these innovations, cash advance apps like MoneyLion have gained significant traction by offering users instant access to funds without the high fees and complexities of traditional payday loans.

As mobile-first financial solutions continue to dominate, with over 70% of users relying on digital platforms for managing their finances, businesses are increasingly investing in scalable lending applications that deliver speed, security, and seamless user experiences.

For Startups and enterprises, this presents a compelling opportunity to build cash advance applications that not only meet growing user expectations but also generate sustainable revenue through innovative fintech models.

However, building a successful app like MoneyLion requires more than just enabling quick payouts. It involves selecting the right technology stack, ensuring regulatory compliance, integrating secure payment systems, and Designing a frictionless user journey.

In this guide, we’ll break down How to build a cash advance app like MoneyLion, including essential features, architecture, Development costs, and monetization strategies to help you launch a competitive fintech product.

What is the MoneyLion App?

The modern personal finance application MoneyLion enables regular people to achieve better financial choices through a banking system that eliminates traditional banking stress. The application serves users who need better financial control to handle their daily expenses and achieve better long-term monetary stability.

The application provides users with secure access to banking services, cash advances, investing options, and credit-building tools, and budgeting analysis. MoneyLion provides users with two essential features, which include Instacash for instant cash advances up to $500 with no interest and Credit Builder Plus for credit score improvement through savings.

MoneyLion provides users with financial tools that extend beyond basic transaction management. The application enables users to track their financial activities and receive individualized advice, which helps them achieve better financial stability.

Users of MoneyLion can invest their small changes and receive alerts about their spending behavior, and earn rewards for making positive financial choices.

MoneyLion has established itself as a reliable digital finance platform, boasting a 10 million-user base and an advanced encryption protection system. The application functions as your financial ally, enabling you to borrow money safely, save money automatically, and invest your funds wisely.

MoneyLion simplifies complicated financial management through its user-friendly interface, which provides users with essential tools to create their ideal financial future.

Best 25+ Cash Advance Apps Like MoneyLion to Download in 202-2026

People experience financial management as an overwhelming task because they need to monitor their spending and make timely payments while building savings and protecting their credit rating. The financial technology sector has developed solutions that simplify financial management for users. Mobile finance applications such as MoneyLion enable users to access borrowing and saving, investment, and credit-building services through their mobile devices.

MoneyLion operates as part of a larger financial application market. Multiple financial applications provide advanced features that serve specific financial requirements, including emergency funding, investment management, and budget control.

The search for MoneyLion alternatives has led you to this platform. Our research identifies the matches MoneyLion’s features to help users achieve better financial control.

Whether you’re looking for:

- A personal loan or cash advance app to cover short-term expenses,

- A budgeting tool to gain better control over your spending, or

- An all-in-one finance app that blends banking, investing, and credit tracking,

There’s an option for everyone.

Below, you’ll find a carefully curated list of the 25+ best apps similar to MoneyLion, complete with their key features and benefits. Take a look, compare their offerings, and pick the one that aligns best with your financial goals.

1. Brigit

Brigit serves as a financial health application that enables users to prevent overdraft fees while tracking their expenses and obtaining emergency cash advances until their next payday. The application provides users with instant financial assistance and advanced money management features, which make it a leading alternative to MoneyLion.

Brigit operates differently from standard loan applications because it enables users to develop improved financial practices through its automated analysis system and budget monitoring capabilities. The system uses predictive technology to detect when your account balance approaches zero so you can stop overdraft fees from happening.

How it works:

- Download & Connect: Install the Brigit app and securely connect it to your bank account.

- Financial Analysis: Brigit analyzes your spending patterns and cash flow to understand your financial health.

- Instant Cash Advance: If you qualify, you can receive up to $250 instantly without interest, credit checks, or hidden fees.

- Automatic Repayment: The borrowed amount is automatically repaid on your next payday.

- Credit Builder & Alerts: Access credit-building tools and get real-time alerts about your balance and upcoming bills.

Pros and Cons of Brigit

| Pros of Brigit | Cons of Brigit |

| Offers instant cash advances up to $250 with no interest or hidden fees | Requires a paid subscription (starting at around $9.99/month) for full features |

| No credit check required to qualify for cash advances | Limited cash advance amount compared to some competitors |

| Helps prevent overdraft fees through predictive balance alerts | Not available for all banks or credit unions |

| Includes a Credit Builder feature to improve your credit score | It may take a few days to qualify for new users |

| Simple, user-friendly interface and quick approvals | No option for larger loans or long-term lending |

| Financial insights and budgeting tools included | Some users report delays in fund transfers during peak times |

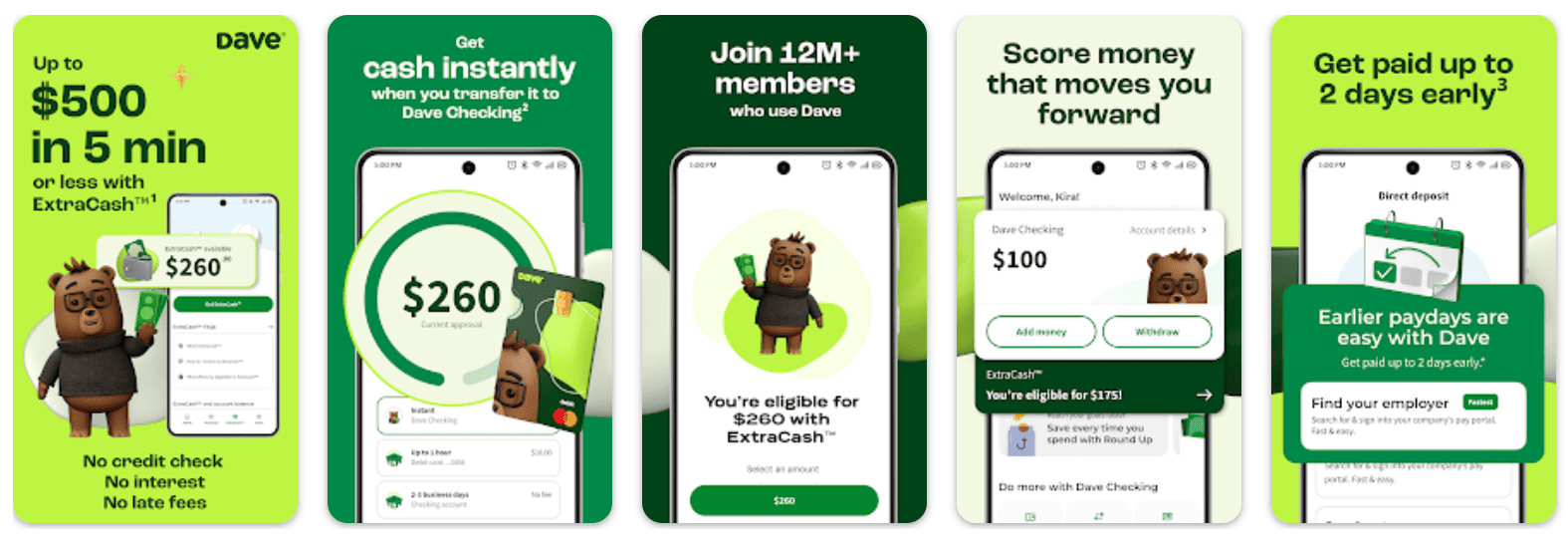

2. Dave

The financial application Dave functions as a trusted cash advance solution, which enables users to prevent overdraft fees while obtaining emergency funds before their next payday. The application provides users with financial flexibility through its combination of personal finance tools and responsible short-term lending services similar to MoneyLion and Brigit.

The application provides users with instant small cash advances while helping them develop credit health through interest-free and feeless transactions. The application provides users with income tracking and job-finding tools and automatic budgeting features to achieve their financial targets.

How it works:

- Sign Up & Connect: Download the Dave app and securely link it to your checking account.

- Budget Analysis: Dave tracks your expenses, upcoming bills, and paydays to forecast potential shortfalls.

- Instant Cash Advance: Eligible users can get up to $500 in advance to cover urgent expenses, with no interest or credit check.

- Repayment: The borrowed amount is automatically deducted from your account once your paycheck is deposited.

- Extra Tools: Access side gigs through the “Dave Extra Cash” feature and track income with personalized financial insights.

Pros and Cons of Dave

| Pros of Dave | Cons of Dave |

| Offers cash advances up to $500 with no interest | Requires a small monthly membership fee (around $1–$2) |

| No credit check required for eligibility | Express delivery for cash advance may incur an additional fee |

| Helps users avoid overdraft fees with predictive balance alerts | Express delivery for a cash advance may incur an additional fee |

| Includes Side Hustle feature to find gig work and earn extra income | Some users report delays in receiving funds during high traffic |

| Automatically tracks expenses and upcoming bills | Requires linking your bank account for full functionality |

| Easy-to-use interface with fast approvals | Repayments are automatic less flexibility in scheduling |

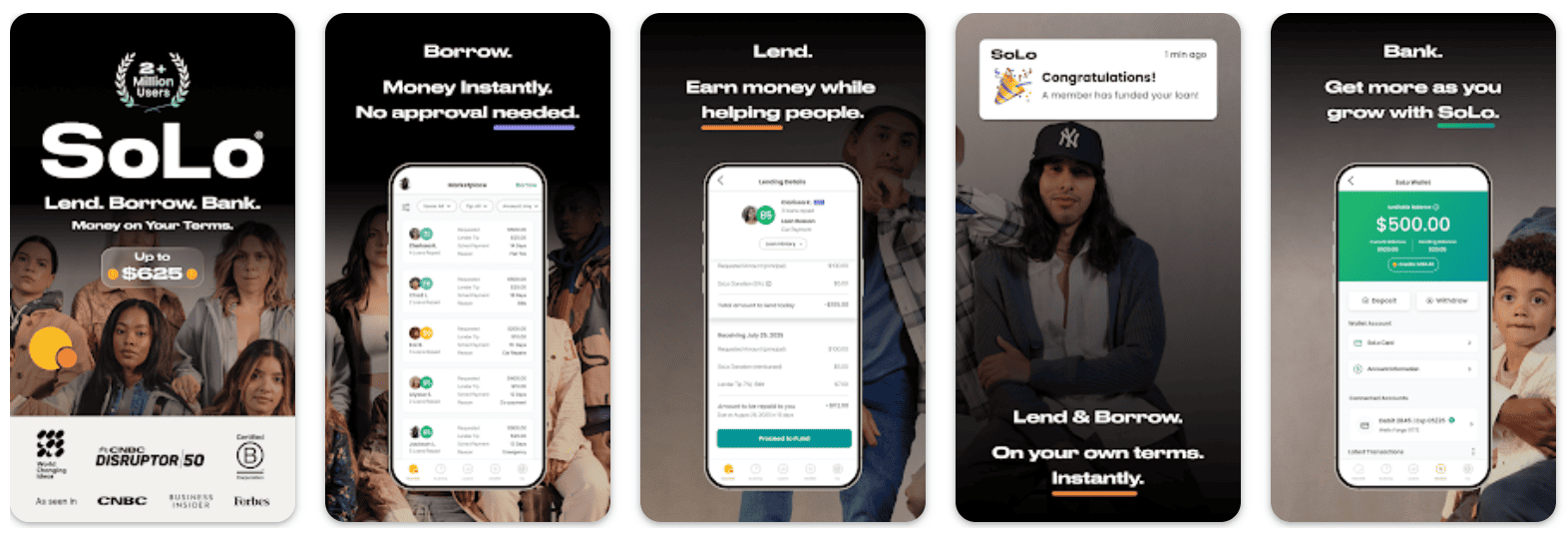

3. SoLoFunds

The peer-to-peer lending application SoLo Funds enables users to obtain short-term loans from lenders through direct connections that bypass conventional banking institutions. The platform enables users to determine their loan conditions and show gratitude to lenders through small tips instead of using credit scores or interest rates.

The platform offers users a better alternative to MoneyLion because it provides flexible and fast borrowing options with complete transparency.

How it works:

- Create an Account: Download the SoLo Funds app and link your verified checking account.

- Request a Loan: Enter the amount you need (usually up to $575), set your repayment date, and choose an optional tip for the lender.

- Get Funded: Once a lender accepts your request, the money is transferred directly to your bank, often within minutes.

- Repay On Time: Repay the loan within the agreed period (typically up to 35 days) to maintain a strong borrower reputation.

- Build Trust: Responsible repayments improve your SoLo Score, increasing your chances of getting funded faster in the future.

Pros and Cons of SoLo Funds

| Pros of SoLo Funds | Cons of SoLo Funds |

| No credit check required, making it accessible for users with poor or limited credit history | Loan repayment period is short (usually 15–35 days) |

| Flexible borrowing terms you choose the amount, duration, and optional tip | Only one active loan is allowed at a time |

| Transparent and community-driven lending model | Flexible borrowing terms, you choose the amount, duration, and optional tip |

| Fast funding loans are often approved and transferred within minutes | Flexible borrowing terms, you choose the amount, duration, and optional tip |

| Helps build a positive borrowing reputation through the SoLo Score | An optional tip may influence Why quickly a loan gets funded |

| No traditional interest or hidden fees | Not ideal for large or long-term financial needs |

4. EarnIn

The payday advance application EarnIn enables users to retrieve their earned wages before their regular payday arrives. The application provides users with a solution to manage unexpected costs through its service, which avoids both high-interest loans and bank overdraft fees.

The service model of EarnIn operates without requiring users to pay interest or mandatory fees because it asks users to decide their service payment amount. Users maintain complete authority to determine their service payment amount through EarnIn’s “tip what you think is fair” system. The financial stability features of EarnIn, including Balance Shield and Tip Yourself, enable users to monitor their spending habits effectively.

How it works:

- Download & Connect: Install the EarnIn app and securely link it to your checking account and employer details.

- Track Your Earnings: The app monitors your work hours or deposits to calculate How much money you’ve earned in real-time.

- Cash Out Instantly: You can withdraw a portion of your earned wages (up to $150 per day or $1,000 per pay period) before payday.

- Automatic Repayment: Once your paycheck is deposited, the borrowed amount is automatically deducted.

- Extra Tools: Use features like Balance Shield to prevent overdrafts and Tip Yourself to build better savings habits.

Pros and Cons of EarnIn

| Pros of EarnIn | Cons of EarnIn |

| No interest or mandatory fees, users pay voluntary “tips” instead | Limited withdrawal amount per day and per pay period |

| No credit check required, accessible for users with low credit scores | Frequent use may lead to dependency between paychecks |

| Helps avoid overdraft fees with the Balance Shield feature | Requires consistent employment and a regular paycheck |

| Includes extra tools for savings and credit monitoring | No credit check required, accessible for users with low credit |

| Simple setup and transparent process | An instant cash-out option may include small processing fees |

| Provides early access to earned wages, ideal for covering urgent expenses | Advance amount eligibility may vary by income and history |

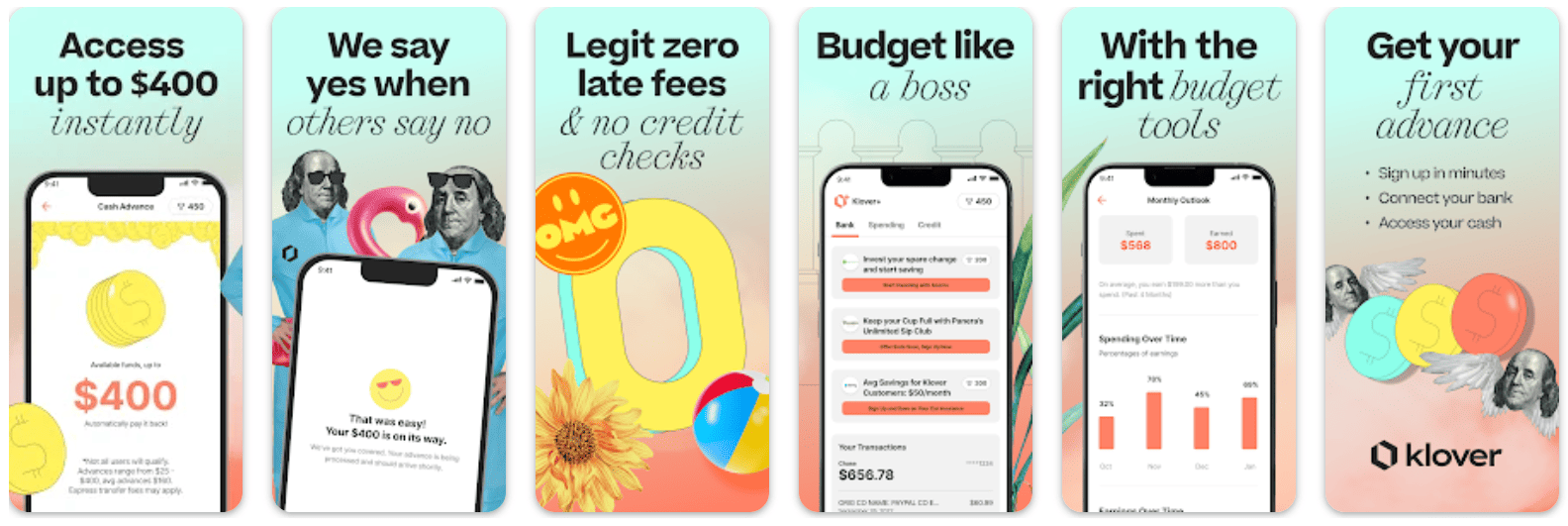

5. Klover

The mobile application Klover provides users with cash advances and financial tools to help them manage their money between paychecks. The application offers users a no-interest, no-credit-check cash advance system together with budgeting tools and reward programs for users who need short-term financial assistance.

How it works:

- Sign Up & Link Account: Download the app and securely link your checking account.

- Verify Eligibility: The app checks your income pattern, direct deposits, and account standing to determine your advance limit.

- Earn Points (Optional): You can complete tasks such as watching videos, scanning receipts, or taking surveys to earn points, which may increase your advance limit or waive fees.

- Request Advance: Based on your limit, you can request a small cash advance (e.g., up to around $200). Standard delivery is free (takes up to a few business days); you may pay a fee for faster transfer.

- Automatic Repayment: The borrowed amount is automatically deducted from your next paycheck or scheduled deposit.

- Budgeting Tools (Optional): You can also opt into a paid upgrade for budgeting tools, spending tracking, credit monitoring, and other features.

Pros and Cons of Klover

| Pros of Klover | Cons of Klover |

| The points system allows you to upsell your advance limit or gain rewards | Advance amounts are relatively low compared to some competitors |

| Standard transfer is free if you wait (no fee) | Instant or expedited transfers incur extra fees |

| Optional budgeting/spend‐tracking tools are available for better money management | The points system can be time‐consuming and complex |

| Optional budgeting/spend‐tracking tools available for better money management | Requires direct deposits and stable income; gig or irregular earnings may not qualify |

| Transparent model emphasizing no hidden interest | You may end up sharing significant personal/financial data or redeeming tasks to boost eligibility |

6. Albert

The finance application Albert provides users with complete financial management through its budgeting and saving, investment, and overdraft protection features. The application unites banking capabilities with automated savings and emergency cash access to let users track their complete financial situation through their mobile device.

How it works:

- Download and link your bank account so Albert can monitor income, spending, and balances.

- Use the budgeting and tracking tools to view your cash flow, upcoming bills, and subscriptions.

- Activate automatic savings: Albert analyzes your transactions and transfers small amounts you can afford into savings.

- Upgrade to the “Genius” tier (optional) to unlock features like the checking-account alternative, debit card with cash-backs, early paycheck access, and cash advances up to around $250.

- When you request a cash advance, the money hits your account and is automatically repaid (typically with your next deposit).

Pros and Cons of Albert

| Pros of Albert | Cons of Albert |

| Access to debit card, cashback rewards, and early payday for eligible users | Many of the advanced features require a paid subscription |

| Automatic savings feature helps build discipline | Savings yield is modest compared to dedicated high-yield accounts |

| Cash advances with no credit check (for qualifying users) | Combines budgeting, saving, investing, and early-cash access in one app |

| Access to debit card, cashback rewards and early payday for eligible users | Access to debit card, cashback rewards, and early payday for eligible users |

| Helps track bills and identify recurring charges to cancel | Users may need to meet direct-deposit/income requirements for full access |

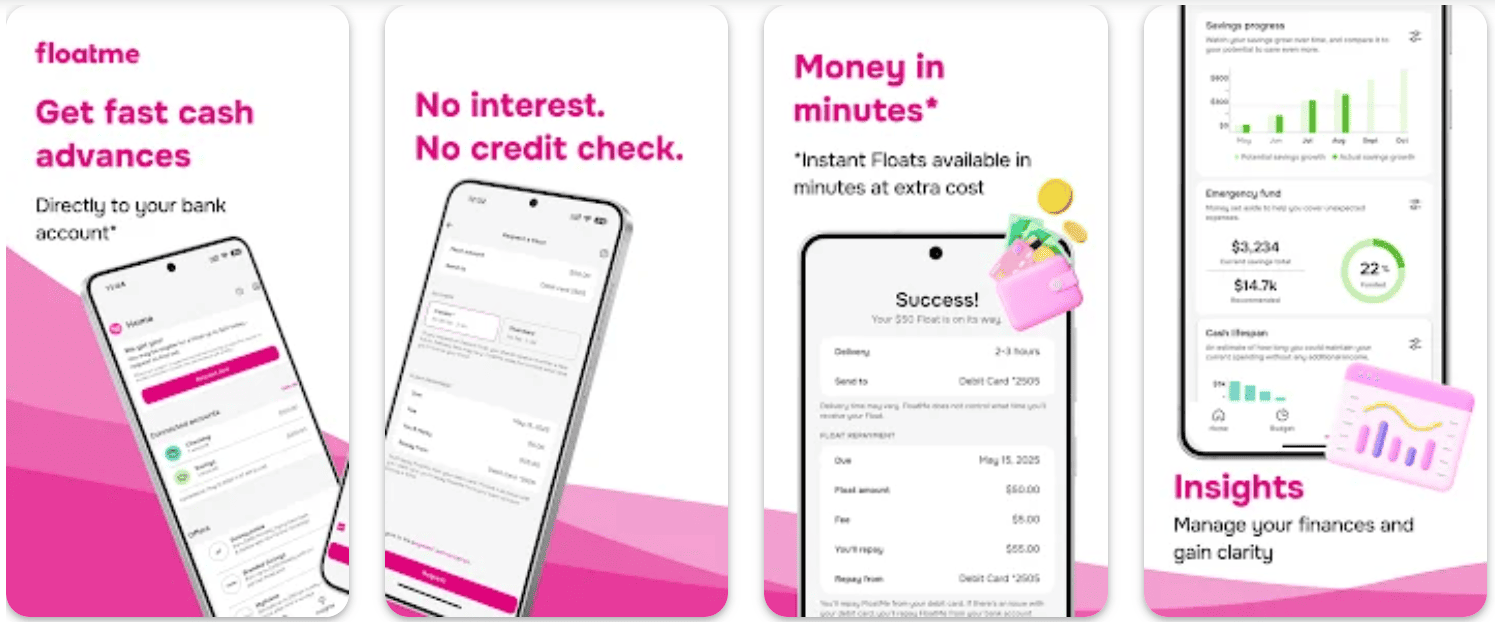

7. FloatMe

The short-term cash-advance application FloatMe provides financial support between paychecks while adding tools to track bank accounts and prevent overdrafts. The application provides users with small financial assistance known as “floats”, which become due after their upcoming paycheck arrives.

How it works:

- Sign up for the app and link your bank account.

- Subscribe to the service (monthly fee applies) to become eligible for floats.

- Request a float amount (usually up to around $50-$100 for new users) when you expect a shortfall before your next income.

- Funds are transferred via standard ACH (1-3 business days), or you can choose an “Instant Float” (typically same day) for an extra fee.

- Pick a repayment date (usually around your payday), and the float + any fees will be debited automatically from your linked account.

- Use the app’s cash-flow calendar and low-balance alerts to track upcoming bills and avoid overdrafts.

Pros and Cons of FloatMe

| Pros of FloatMe | Cons of FloatMe |

| No interest on advances, you pay a fee or subscription rather than traditional loan interest | Monthly membership fee plus potential instant-funding fees add cost |

| Helps avoid overdraft fees by giving early short-term access to cash | Advance amounts are very small compared to some competitors |

| No interest on advances, you pay fee or subscription rather than traditional loan interest | Requires subscription; not free to use its full features |

| Simple application process; no credit check required for floats | Some users report restrictive eligibility, and recent regulatory issues regarding advertising |

| Helpful for users with tight cash flow between paychecks | Not suited for large or longer-term borrowing needs; could reinforce dependency on short advances |

8. Chime

The mobile banking application Chime provides users with affordable banking solutions through its user-friendly interface. The banking service of Chime provides users with fee-free banking because it does not charge monthly fees and maintains no minimum balance requirements while offering tools to help customers save money and prevent overdraft fees.

How it works:

- Download the Chime app, create an account by providing basic personal details, link your checking account, or set up direct deposit.

- Once your account is active, you’ll receive a Chime debit card and access a checking account plus optional savings features.

- Deposit funds via direct deposit, bank transfer, or cash deposit at participating retailers.

- Use the Chime app to track spending, set up automatic savings, and use features like fee-free overdraft (“SpotMe”) if eligible.

- Enjoy additional perks like getting your paycheck deposited early when you qualify, and mobile banking tools for managing your money on the go.

Pros and Cons of Chime

| Pros of Chime | Cons of Chime |

| No monthly service fee, no minimum balance requirement | Some features (like overdraft protection or early pay) require direct deposit and eligibility |

| Fee-free in-network ATM access and no overdraft fees under certain conditions | Out-of-network ATM or cash deposit may incur fees from third parties |

| Built-in automatic savings tools and simple budgeting interface | As a neobank, limited branch access (mobile only) and may rely on partner banks |

| Ability to receive paycheck early when qualifying via direct deposit | Some users report issues with customer service or account closures in edge cases |

| Ability to receive a paycheck early when qualifying via direct deposit | Users should verify FDIC insurance via partner banks fintech model differs from traditional banks |

9. Empower

The financial application Empower enables users to track their budget and net worth while providing savings features and access to cash or credit advances in certain situations. The application enables users to connect various financial accounts, which displays their complete financial situation while helping them establish targets for better money management.

How it works:

- Download Empower and link your checking, savings, investment, and other accounts to the dashboard.

- The app aggregates your financial data and presents an overview of your spending, net worth, savings goals, and possible debt pay-down opportunities.

- Use the budgeting and cash-flow tools to set targets, monitor where your money is going, and receive insights or alerts.

- If available, you may access features like high-yield cash accounts, early wage access, or credit/advance products (depending on offers and eligibility).

- Review progress toward goals (retirement, emergency fund, debt pay-off), adjust your plan, and use the app’s guidance to steer your finances.

Pros and Cons of Empower

| Pros of Empower | Cons of Empower |

| Some advanced features may require a subscription or eligibility (not purely free) | Some advanced features may require subscription or eligibility (not purely free) |

| Helps you set and monitor budgets, savings goals, and track net worth | Budgeting features may be less granular in categories compared to some competitors |

| Potential access to high-yield cash accounts and financial tools | Some users may feel overwhelmed by too many linked accounts or data entry |

| Good for long-term financial planning, not just short-term cash fixes | Not strictly a payday advance app may not help with immediate emergency cash needs |

| Comprehensive financial dashboard: view all your accounts in one place | Linking multiple accounts raises security/data concerns for some users |

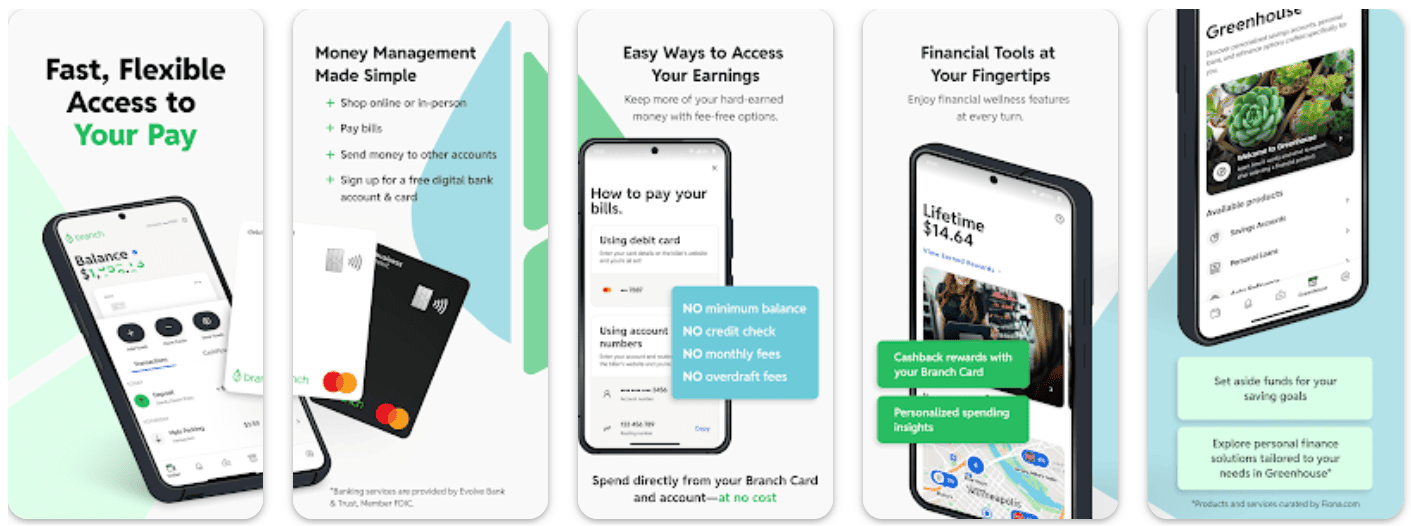

10. Branch

The mobile application Branch provides users with earned-wage access, a digital wallet, and banking functionality. The application enables users who work hourly or as gig workers to access their earned wages before payday while providing tools for pay management, direct deposit services, and digital debit card access. The platform provides users with early access to their earned wages through a more flexible system than traditional payday loans.

How it works:

- Download the Branch app and create your account, linking your employer/payroll (if required) and setting up your Branch wallet.

- Within the app, you will see an available advance amount (based on your eligible earned wages). Select the “Take Advance” or equivalent option.

- Confirm the amount and repayment date; the funds will be deposited into your Branch wallet or bank account immediately.

- Use the Branch debit card/wallet to spend, save, or transfer funds; savings and financial wellness tools may also be available.

- When your next paycheck arrives or when repayment is due, the advance is settled. Branch offers this as a more flexible alternative to high-cost payday loans.

Pros and Cons of Branch

| Pros of Branch | Cons of Branch |

| Advance limits depend on the employer setup, and your eligibility may be limited | If used repeatedly, it may create dependency on wage advances rather than budgeting |

| Allows access to wages you’ve already earned, helps bridge cash-flow gaps without traditional payday loan rates | Since it’s not a full bank, features like FDIC insurance may depend on the underlying partner bank |

| More affordable alternative to payday loans in many cases | Some transfers (e.g., instant out-of-wallet transfers) may incur fees |

| Good tool for workers with irregular pay or hourly jobs needing access to funds before payday | Not all employers support integration or enable full access to wage advances |

| Includes savings and financial tools alongside pay access | Since it’s not a full bank, features such as FDIC insurance may depend on the underlying partner bank |

11. Affirm

The “Buy Now, Pay Later” (BNPL) app Affirm lets users make purchases that they can divide into multiple smaller payments over time without facing any unexpected costs. The platform provides users with a better shopping experience than credit cards and personal loans because it offers complete payment transparency. Users can shop immediately through Affirm while paying later without facing any unexpected costs.

Through its partnership with thousands of online and physical stores, Affirm enables users to access various financing plans that match their spending capabilities. Users can obtain instant credit decisions through Affirm, which enables them to select between interest-free short-term plans and extended monthly payment options for their purchases of electronics and furniture, and travel packages.

How it works:

- Shop and Select Affirm: Choose your favorite store and select Affirm as the payment method at checkout.

- Instant Approval Decision: Enter basic details and get an immediate eligibility decision, no long forms or hard credit checks.

- Choose Your Payment Plan: Pick between short-term (biweekly) or long-term (monthly) installment options based on your budget.

- Complete Your Purchase: Affirm pays the merchant upfront, and you pay Affirm back over time.

- Make Payments Easily: Manage your repayments in the Affirm app. You can pay manually or set up auto-pay for convenience.

Pros and Cons of Affirm

| Pros of Affirm | Cons of Affirm |

| Transparent payment structure no hidden fees or surprises | Interest rates can go up to 36% on longer-term plans |

| Offers interest-free payment options for eligible purchases | Missed payments may negatively affect your credit score |

| No late fees or prepayment penalties | Approval amount and terms depend on your credit and spending habits |

| Instant decisions at checkout for faster purchases | Not every store or merchant accepts Affirm |

| Flexible payment terms from 4 biweekly to 60-month plans | Encourages impulse buying if used frequently |

| User-friendly app interface with detailed payment tracking | Multiple ongoing plans can make budgeting harder to manage |

12. AfterPay

The Buy Now, Pay Later (BNPL) app Afterpay lets users split their purchases into interest-free payment installments. The platform lets users make immediate purchases through flexible payment plans, which function as an alternative to credit cards and conventional loans.

The platform operates with more than 1000 retailers worldwide who provide their products through digital channels and brick-and-mortar locations. Users can establish purchase budgets through Afterpay because the platform displays all payment information before they need to make a payment, unless they fail to meet a payment deadline.

How it works:

- Shop with Afterpay: Choose a participating retailer and select Afterpay at checkout.

- Quick Sign-Up: Create an account or log in using your existing Afterpay credentials; no long approval process required.

- Split the Payment: The total cost of your purchase is divided into four equal payments, due every two weeks.

- Instant Checkout: Pay the first installment immediately, and Afterpay covers the rest to the merchant.

- Pay Over Time: Manage your payments easily in the Afterpay app and set reminders or auto-pay to avoid late fees.

Pros and Cons of Afterpay

| Pros of Afterpay | Cons of Afterpay |

| Interest-free payments with no hidden fees | Late or missed payments can lead to extra charges |

| No credit check required to start using the service | Limited spending limits for new users until payment history improves |

| Available at thousands of online and in-store retailers | Frequent use may encourage overspending or impulse buying |

| Quick approval and easy integration during checkout | Payments are automatically deducted less flexibility in scheduling |

| User-friendly mobile app to track purchases and upcoming payments | Not suitable for large, high-value purchases or long-term financing |

| Helps improve budgeting by splitting costs into smaller parts | Missing payments may affect eligibility for future purchases |

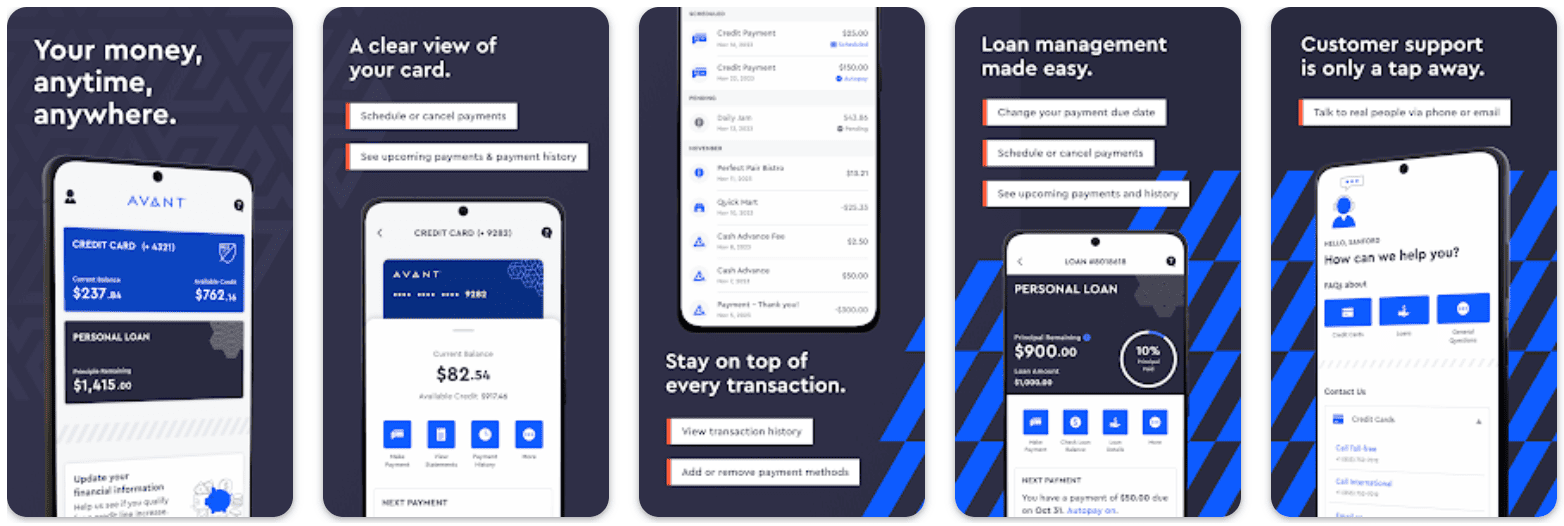

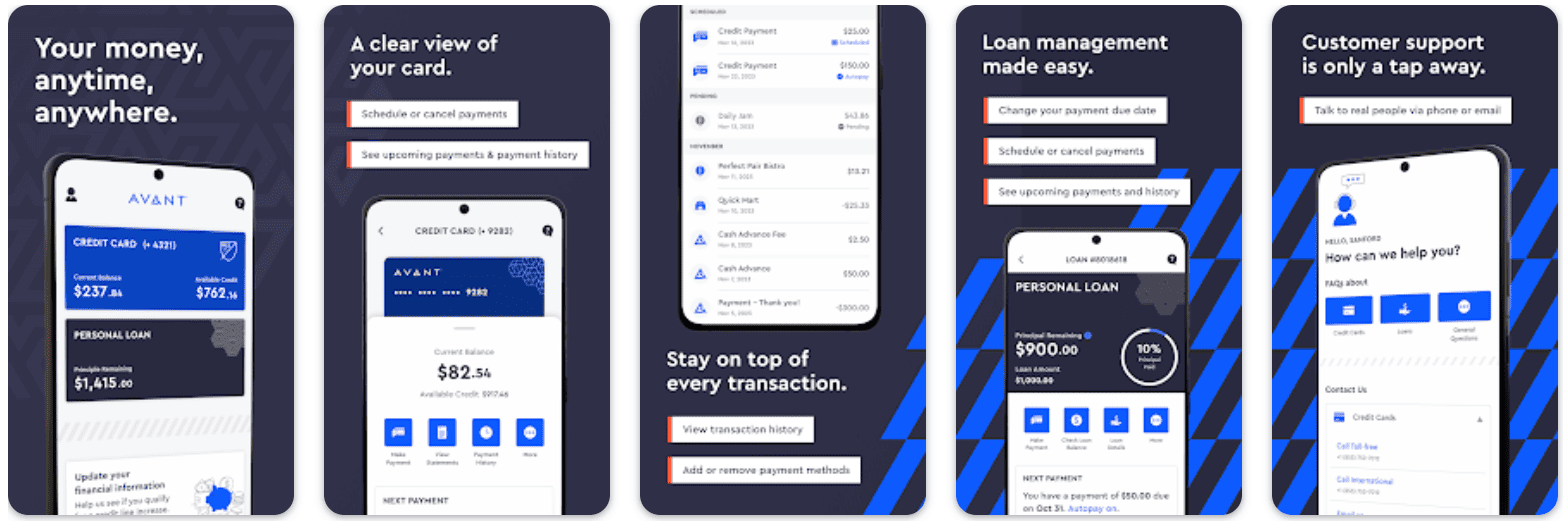

13. Avant

The financial platform Avant offers personal loans and credit cards to users who need immediate access to straightforward financial products. The platform serves users who have fair to good credit since they cannot obtain bank loans through regular channels. The platform offers users flexible payment terms and fast processing, as well as competitive interest rates, which make it an excellent choice for personal financial management.

How it works:

- Apply Online: Visit the Avant app or website and fill out a quick application with basic financial details.

- Get Instant Decision: Avant performs a soft credit check to determine your eligibility and loan amount.

- Review Loan Terms: Choose your preferred repayment plan and confirm your loan agreement.

- Receive Funds: Approved users typically get funds deposited directly into their bank accounts within one business day.

- Repay Over Time: Make fixed monthly payments through the Avant app or via automatic bank withdrawals.

Pros and Cons of Avant

| Pros of Avant | Cons of Avant |

| Fast loan approval and quick fund disbursement | Interest rates can be higher for lower credit scores |

| Suitable for borrowers with fair to good credit | Charges an administrative or origination fee on some loans |

| Fixed repayment terms make budgeting easier | Not available in all U.S. states |

| Offers both personal loans and credit cards | Missed payments may incur late fees |

| Option to prepay loans early without penalties | Limited maximum loan amount compared to traditional lenders |

14. Axos Bank

Axos Bank operates as a digital banking institution that provides complete financial solutions through its digital platform. The bank provides personal and business checking services alongside high-yield savings accounts, loan options, and investment products. The bank provides users with digital banking convenience through its secure platform, which offers competitive interest rates. Users who want to manage their finances through a single Digital platform should choose this bank.

How it works:

- Open an Account: Visit the Axos website or app and choose from checking, savings, or business account options.

- Verify Identity: Complete a secure online verification process to activate your account.

- Deposit Funds: Add money to your account via direct deposit, mobile check deposit, or transfers.

- Manage Through App: Use the Axos app to pay bills, transfer money, and monitor transactions in real time.

- Access Additional Products: Apply for personal loans, auto loans, or mortgages directly through the platform.

Pros and Cons of Axos Bank

| Pros of Axos Bank | Cons of Axos Bank |

| 100% Digital — no need to visit a physical branch | No physical locations for in-person service |

| Offers multiple account types with competitive interest rates | Customer service can be slow during peak hours |

| Fee-free checking options with unlimited domestic ATM reimbursements | Requires online account management may not suit traditional users |

| Strong security features and 24/7 mobile banking access | Some specialized accounts require higher minimum balances |

| Offers personal loans, business banking, and investment options | Limited international banking features |

15. Ingo Money

The mobile application Ingo Money enables users to deposit checks immediately through their device instead of needing to go to a bank or ATM. The application serves freelancers and gig workers and all people who receive paper checks regularly, because it provides quick access to their money. Users can deposit their funds through Ingo Money into their bank account, PayPal, or prepaid card for maximum convenience and speed.

How it works:

- Download the App: Install the Ingo Money app and sign up with your verified ID and payment account details.

- Take Photos of Your Check: Snap clear front and back photos of the check you want to deposit.

- Choose Why to Get Paid: Decide whether you want a standard deposit (1–5 days, free) or an instant deposit (minutes, with a small fee).

- Submit for Review: Ingo verifies your check and processes the payment securely.

- Access Your Money: Approved funds are transferred directly to your chosen account or card.

Pros and Cons of Ingo Money

| Pros of Ingo Money | Cons of Ingo Money |

| Offers instant check deposits without visiting a bank | Instant deposits may include processing fees |

| Works with bank accounts, PayPal, and prepaid cards | Not all check types are eligible (e.g., handwritten checks) |

| Fast, secure, and easy to use for freelancers and gig workers | Standard deposits take several business days |

| Provides flexibility in Why users receive their funds | Daily and monthly check amount limits apply |

| Reduces dependency on physical banks or ATMs | Rejected checks may cause temporary account holds |

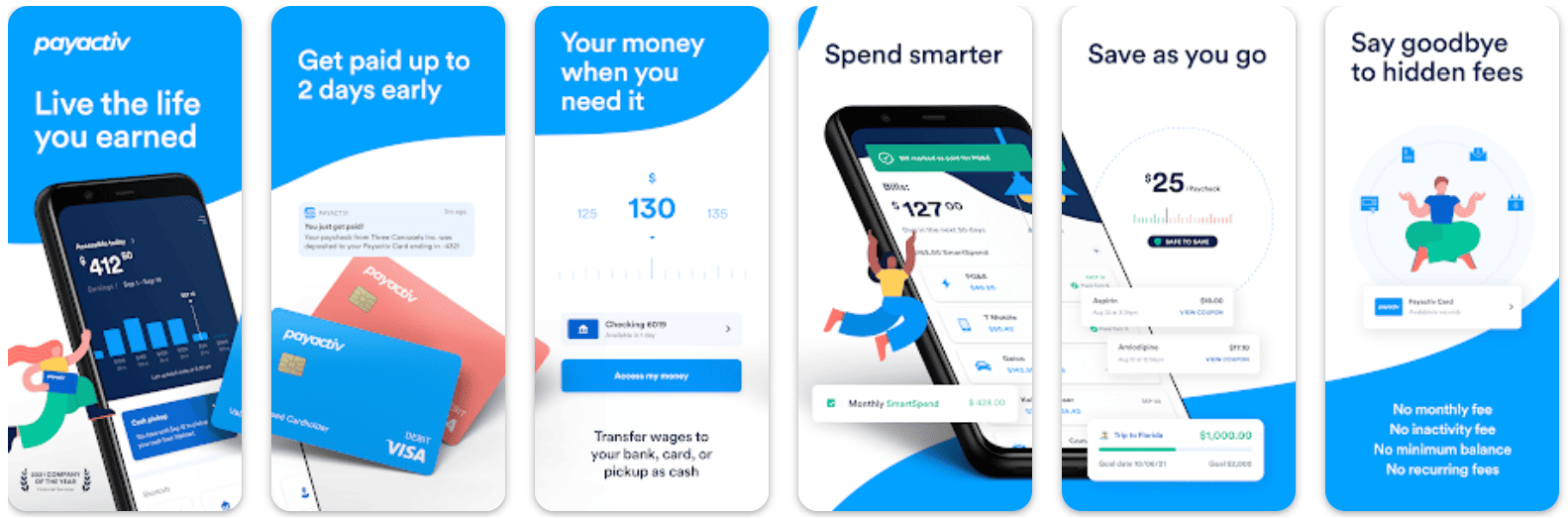

16. Payactiv

The financial wellness application Payactiv enables workers to access their earned wages through EWA before their regular payday arrives. The application enables employees to access their earned wages before payday while reducing financial stress and eliminating payday loan and overdraft fee requirements. The platform provides on-demand pay services together with budgeting tools, bill payment options, savings features, and a prepaid debit card for complete employee financial management.

How it works:

- Sign Up and Link Employment:

Download the Payactiv app and connect your account with your employer or verify your payroll details. - Track Earned Wages:

The app automatically tracks the hours you’ve worked and shows How much of your earned wages are available to withdraw. - Access Your Funds:

You can choose to receive your earned pay through direct deposit, the Payactiv Visa Card, instant bank transfer, or even cash pickup. - Automatic Repayment:

When your next paycheck arrives, the advanced amount is automatically deducted, so there’s no need to manually repay it. - Use Built-In Tools:

Manage your finances better with Payactiv’s extra tools like savings goals, automatic budgeting, bill reminders, and discount offers.

Pros and Cons of Payactiv

| Pros of Payactiv | Cons of Payactiv |

| Access earned wages instantly without waiting for payday | Full features may not be available unless your employer partners with Payactiv |

| No credit check or interest charges | Small fees may apply for instant transfers or cash withdrawals |

| Helps avoid payday loans, overdraft fees, and financial emergencies | Overusing earned wage access can disrupt long-term budgeting |

| Offers budgeting, saving, and bill payment tools in one app | Limited access to wages (typically up to 50% of earned pay) |

| Supports various payout options including debit card and bank transfer | Requires stable employment for continuous access to EWA services |

| Encourages financial discipline with savings and goal-setting features | Supports various payout options, including debit card and bank transfer |

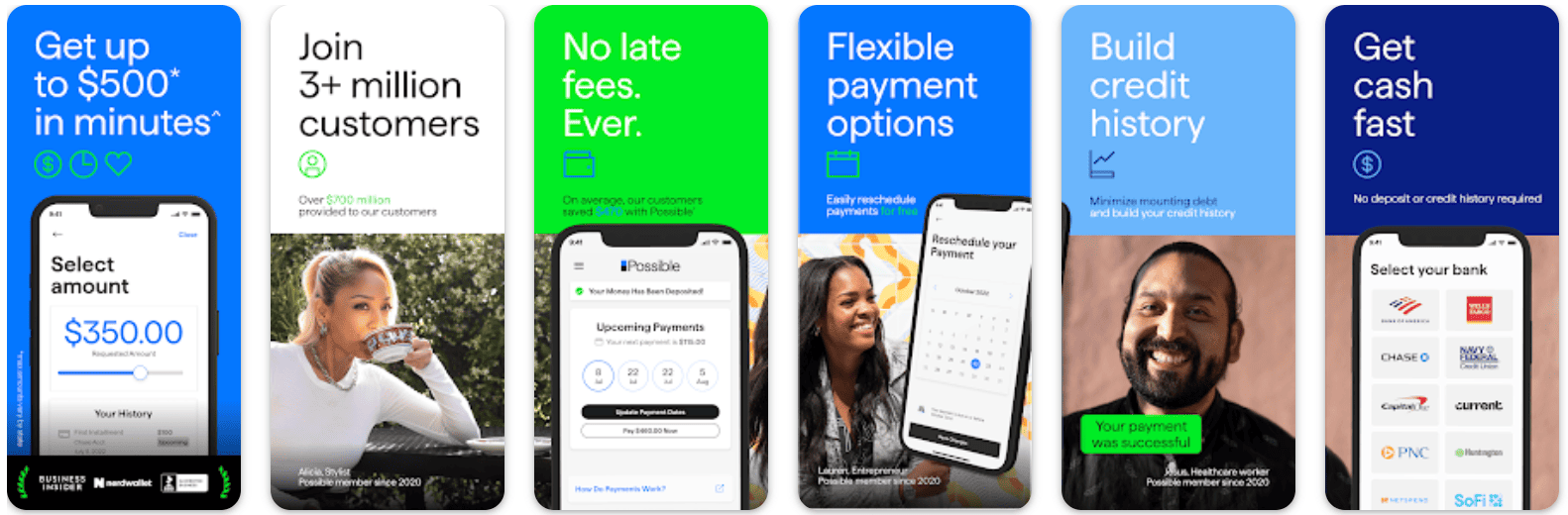

17. Possible Finance

The mobile application Possible Finance provides users with accessible short-term loans at affordable rates, which surpass the high costs of conventional payday loans. The application provides financial assistance to users who lack a credit history by offering instant loans, which help them construct their credit profile. The application provides users with adaptable payment options and complete transparency about all costs so they can replace payday loans with a responsible financial solution.

How it works:

- Apply via the mobile App:

Download the app, create an account, and provide basic personal and banking information. - Get Instant Loan Approval:

The app evaluates your financial history and spending patterns, not just your credit score, to determine eligibility. - Receive Funds Quickly:

Approved loans are typically deposited into your linked bank account within a few hours or the next business day. - Repay Over Time:

Repay your loan in multiple installments over several weeks with no penalties for early repayment. - Build Your Credit:

On-time payments are reported to credit bureaus, helping improve your credit score gradually.

Pros and Cons of Possible Finance

| Pros of Possible Finance | Cons of Possible Finance |

| Accessible to users with poor or limited credit history | Interest rates can be higher than traditional loans |

| Reports payments to credit bureaus to help build credit | Loan availability varies by state |

| Flexible installment repayment options | Short-term loan amounts are relatively small |

| No late fees or prepayment penalties | Limited customer support during weekends |

| Fast and easy mobile application process | Must connect your bank account for eligibility |

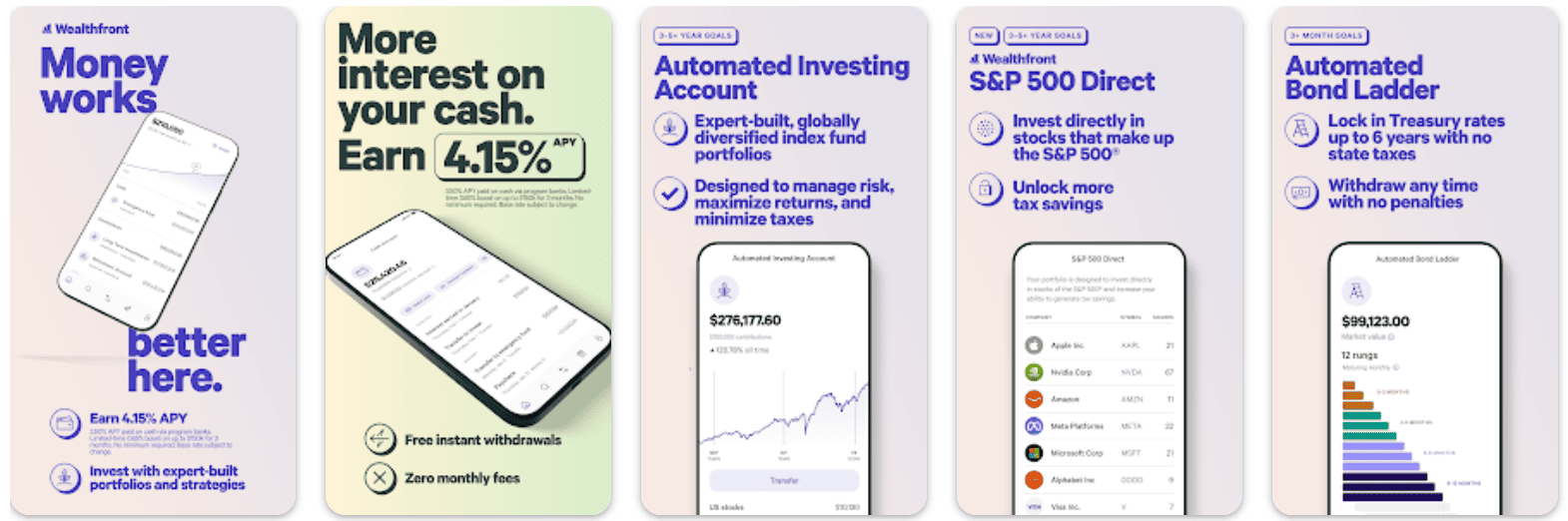

18. Wealthfront

Wealthfront operates as an automated investment platform that enables users to build their wealth through sophisticated algorithms that require minimal user involvement. The application provides users with investment management services and high-interest savings options, and automated financial planning capabilities through a single platform. The platform serves users who want to invest their money without direct involvement while achieving maximum financial growth through intelligent management.

How it works:

- Sign Up and Set Goals:

Create a Wealthfront account and define your financial goals (retirement, saving, investing, etc.). - Automated Portfolio Creation:

Wealthfront builds a personalized, diversified investment portfolio using ETFs based on your risk tolerance. - Automatic Rebalancing:

The system automatically adjusts your portfolio to keep it aligned with your financial goals and market conditions. - Earn on Cash:

Deposit cash into your Wealthfront account to earn a competitive interest rate with no account fees. - Monitor and Grow:

Track your investments and goals easily through the app while Wealthfront handles all the complex management in the background.

Pros and Cons of Wealthfront

| Pros of Wealthfront | Cons of Wealthfront |

| Fully automated investment management | Limited customer support compared to traditional advisors |

| No account minimum for cash accounts | Does not offer human financial advisors |

| Low management fees (around 0.25%) | Limited customization for portfolios |

| Offers tax-loss harvesting to save on taxes | Investment options limited to ETFs |

| High-yield savings account available | Not ideal for active traders or short-term investors |

| Intuitive app with easy financial goal tracking | May feel impersonal for those preferring hands-on control |

19. Revolut

Revolut operates as a worldwide financial super app that provides users with banking services and currency exchange capabilities, investment tools, and budget management features through a single interface. Users can maintain different currencies through Revolut, which enables them to perform currency exchanges and money transfers at actual market rates. The platform serves travelers and digital nomads who require instant international money transfers without paying excessive conversion costs.

How it works:

- Create a Revolut Account:

Download the app, verify your identity, and set up your Revolut account in minutes. - Add Funds and Choose a Plan:

Add money using your bank account or card and select between Standard (free) or Premium/Metal paid plans for additional perks. - Spend and Transfer Globally:

Use your Revolut card for payments, ATM withdrawals, or instant transfers all at interbank exchange rates. - Manage Your Finances:

Track spending, set budgets, and use built-in analytics to understand your expenses. - Invest or Save:

Access features like stock and crypto investing, savings vaults, and cashback rewards within the same app.

Pros and Cons of Revolut

| Pros of Revolut | Cons of Revolut |

| Real-time currency exchange at interbank rates | Foreign transaction fees may apply outside the included limits |

| Supports multiple currencies and countries | The free plan has withdrawal and exchange limits |

| Includes stock, crypto, and commodities trading | Customer support response times can be slow |

| Built-in tools for budgeting and analytics | Cash deposits and check handling not supported |

| Secure transactions with disposable virtual cards | Cash deposits and check handling are not supported |

| Great for frequent travelers and freelancers | Not a replacement for a full-service bank in some countries |

20. Varo

The mobile banking application Varo provides users with a contemporary solution to handle their financial needs through its user-friendly interface. The application provides users with fee-free services and early direct deposit access, automatic savings features, and cash advance options to create a mobile banking experience that surpasses traditional banking institutions. The platform provides users with credit-building features and high-yield savings options, which make it perfect for individuals who want to achieve financial freedom and improve their money management skills.

How it works:

- Sign Up & Open an Account:

Download the Varo app, verify your identity, and open a free online bank account within minutes. - Direct Deposit & Manage Money:

Link your paycheck to Varo and enjoy early access to funds (up to two days before payday). - Access Cash Advances:

Use the Varo Advance feature to borrow small amounts based on your account activity and repayment history. - Save Automatically:

Set up Auto-Save rules that move money into your savings account each time you get paid or make a purchase. - Build Credit:

Enroll in Varo Believe, a credit-building program that reports timely payments to major credit bureaus.

Pros and Cons of Varo

| Pros of Varo | Cons of Varo |

| No hidden banking fees or overdraft charges | Cash advances limited based on account behavior |

| Early access to direct deposits (up to 2 days sooner) | Customer support may take time to resolve issues |

| High-yield savings accounts for better returns | No physical bank branches for in-person services |

| Credit-building program (Varo Believe) available | Some premium features may require consistent deposits |

| Easy-to-use mobile app with budgeting tools | Limited to U.S. residents only |

21. Avant Credit

The personal loan application Avant Credit enables users who have fair to good credit scores to obtain quick funding through a simple approval system. The platform provides users with personal loans and credit cards and adaptable payment options that match their specific financial requirements. The platform provides users with clear loan costs and fast processing times, which suits people who need to merge debts or handle unexpected situations, or support personal initiatives.

How it works:

- Apply Online:

Fill out a short application form through the Avant app or website, no paperwork required. - Instant Offer Preview:

Get a quick loan offer showing your potential amount, APR, and repayment terms without affecting your credit score. - Accept and Receive Funds:

Once approved, funds are deposited directly into your bank account as soon as the next business day. - Repay Flexibly:

Manage monthly payments easily through the app and even pay off early without penalties. - Monitor Credit Health:

Track your credit score and payment progress through Avant’s dashboard.

Pros and Cons of Avant Credit

| Pros of Avant Credit | Cons of Avant Credit |

| Quick and simple online loan application process | Interest rates can be higher for lower credit scores |

| Soft credit check for initial offer | Charges an administration or origination fee on some loans |

| Fast approval and next-day funding | Not ideal for users with very poor credit history |

| No prepayment penalties for early payoff | Late payment fees may apply |

| Provides both personal loans and credit cards | Not ideal for users with a very poor credit history |

22. Cleo

Cleo operates as a financial assistant application that enables users to monitor their expenses and build savings while enhancing their budgeting capabilities through its interactive chat system. The financial assistant Cleo functions as a budgeting companion that uses automated tools and personal financial insights to help users control their money better, develop saving practices, and obtain emergency cash access.

How it works:

- Connect Your Bank Accounts:

Sign up on the Cleo app and securely connect your bank to allow the AI assistant to analyze your spending. - Get Smart Budgeting Tips:

Cleo helps categorize expenses, identifies spending habits, and suggests saving opportunities. - Access Cash Advances:

Eligible users can request small advances instantly (without traditional credit checks). - Earn Rewards & Build Credit:

Use Cleo’s cashback offers and credit builder tools to strengthen financial health over time. - Engage via Chat:

Interact with Cleo in a conversational tone, ask about your budget, savings, or even get roasted for overspending!

Pros and Cons of Cleo

| Pros of Cleo | Cons of Cleo |

| Fun and interactive AI chat interface for money management | Requires access to banking data, which some users may find intrusive |

| Offers budgeting, savings, and spending insights in one place | Cash advance eligibility depends on spending behavior |

| Instant cash advances without credit checks | Some advanced features are locked behind a Cleo Plus subscription |

| Credit-building tools available for improving financial health | Not ideal for users seeking large loans or financing |

| Easy-to-understand visual reports and spending breakdowns | Humor-based interface may not appeal to all users |

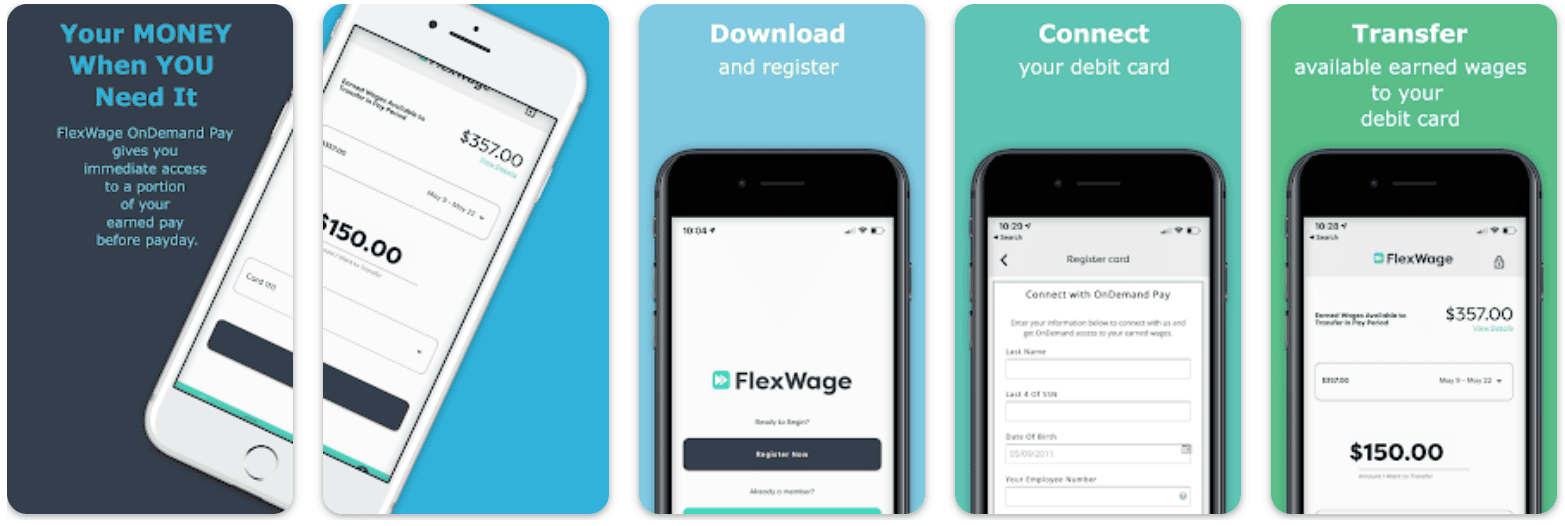

23. FlexWage

The earned wage access platform FlexWage enables employees to access their earned wages before their regular payday, thus creating financial stability and preventing payday loan usage. The platform serves both employers and employees through its digital payment system, which enables workers to manage financial emergencies while organizations support their staff members’ financial health.

The platform FlexWage operates differently from typical lending applications because it does not offer loan services. Through FlexWage, employees can retrieve their already earned wages, which prevents them from facing overdrafts and late payment fees, and financial difficulties.

How it works:

- Employer Partnership Setup:

FlexWage partners with businesses to integrate the platform into their payroll systems. Employees must work for a participating employer to access benefits. - Employee Enrollment:

Employees sign up through their company’s FlexWage portal or app, linking their work profile and verifying their details. - Access Earned Wages:

Based on hours worked, employees can access a portion of their earned pay instantly without waiting for payday. - Instant Transfer:

Funds are transferred to the employee’s linked FlexWage card or bank account in real time, depending on their preferences. - Automatic Deduction:

The advanced amount is automatically deducted from the next paycheck, ensuring seamless repayment.

Pros and Cons of FlexWage

| Pros of FlexWage | Cons of FlexWage |

| Provides early access to earned wages, reducing reliance on payday loans | Only available through participating employers |

| Helps employees manage short-term financial needs responsibly | Not all employees may be eligible depending on employer settings |

| Not all employees may be eligible, depending on employer settings | May include small transaction or access fees based on usage |

| Encourages better financial habits with budgeting tools and resources | Limited flexibility if employer participation ends |

| Employers benefit from improved retention and workforce satisfaction | Access limits may apply based on earnings and work hours |

| Fast and secure fund transfers through prepaid card or direct deposit | No credit checks or interest charges; funds are from earned income |

24. CASHe

The Indian personal loan and credit application CASHe offers instant short-term financial assistance to salaried workers who need emergency funding. The application serves as a financial solution that enables users to obtain loans for their rent payments, utility bills, shopping needs, and unexpected expenses. The Social Loan Quotient (SLQ) algorithm of CASHe evaluates borrowers through their income and social activities, and financial management skills to provide fast loan approval without requiring banking procedures.

Young professionals choose CASHe as their top financial application because it offers flexible repayment options, immediate funding, and clear payment terms.

How it works:

- Download and Register:

Install the CASHe app, sign up using your mobile number, and complete KYC verification with basic documents like ID proof and salary slips. - Check Eligibility:

The app calculates your Social Loan Quotient (SLQ) to determine your eligible loan amount and terms based on your income and profile. - Select Loan Amount and Tenure:

Choose the loan amount you need (from small cash advances to higher-value personal loans) and select your preferred repayment duration. - Instant Approval and Disbursal:

Once approved, the loan amount is credited to your bank account, often within minutes. - Repay Easily:

Repay through the app using convenient payment methods. You can also track EMIs and view your repayment schedule in real time.

Pros and Cons of CASHe

| Pros of CASHe | Cons of CASHe |

| Instant personal loans with quick approval and disbursal | Available only for salaried professionals |

| Late repayment can lead to additional charges or an impact on your credit score | Interest rates may be higher than traditional bank loans |

| Flexible repayment options from a few days to several months | Late repayment can lead to additional charges or credit score impact |

| Uses Social Loan Quotient for faster eligibility decisions | Loan eligibility depends on consistent income and credit behavior |

| No collateral required, completely unsecured loans | Limited availability to users in certain regions of India |

| Provides other features like Buy Now Pay Later and Credit Line | May not suit self-employed or freelancers seeking credit |

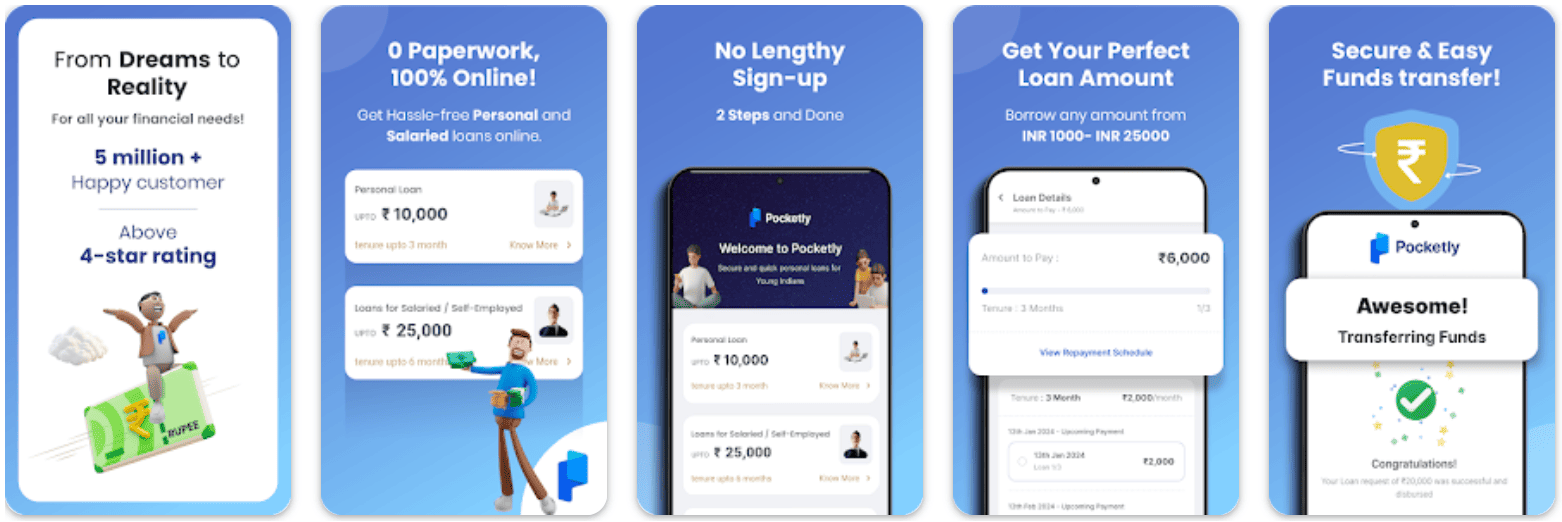

25. Pocketly

The instant personal loan application, Pocketly, serves students and young Indian professionals who need access to quick financial help. The platform enables users to obtain brief loans, which help them handle their regular costs and unexpected situations. The application process at Pocketly remains easy while its fast approval system delivers instant bank account deposits of small loans.

The application helps new credit users practice responsible borrowing through its ability to provide small loans with adjustable payment terms, which serve as an alternative to bank loans for ineligible applicants.

How it works:

- Register on the App:

Download Pocketly from the Play Store or App Store and sign up with your mobile number and basic KYC details. - Complete Verification:

Upload essential documents such as ID proof, PAN card, and student/employment information for quick verification. - Check Eligibility and Apply:

Based on your profile, the app shows your eligible loan limit. Choose the loan amount and repayment period that suits your needs. - Get Instant Disbursal:

Once approved, funds are transferred directly to your bank account, often within minutes. - Repay and Improve Credit Score:

Repay your loan through the app using UPI, debit card, or net banking. Timely repayments help you build your credit score.

Pros and Cons of Pocketly

| Pros of Pocketly | Cons of Pocketly |

| Instant small-ticket loans for students and professionals | Loan limits are relatively low for first-time users |

| Quick online application and instant disbursal | Available only in select regions of India |

| No credit history required for eligibility | High interest for longer tenures |

| Simple KYC and easy-to-use app interface | Late payments can lead to penalties and credit score drop |

| Helps build a credit profile through responsible borrowing | Not ideal for users needing large personal loans |

26. Rufilo

Rufilo operates as a credit line application that offers instant personal loans to employees and self-employed workers who need fast access to credit. The application enables users to request a credit line that functions as a revolving account, which allows them to access funds at any time while paying interest only on the amount they use.

The platform delivers convenient services through its immediate approval process, reduced paperwork requirements, and quick funding delivery. The platform serves as an intelligent financial solution that helps users handle their brief financial needs and unexpected situations and money shortages through alternative funding options beyond payday loans.

How it works:

- Download and Register:

Install the Rufilo app, sign up with your phone number, and complete your profile. - Submit KYC and Income Proof:

Upload documents like PAN, Aadhaar, and income proof for quick verification. - Get Credit Line Approval:

Based on your credit score and financial profile, Rufilo approves a personal credit line (up to your eligible limit). - Withdraw Instantly:

Withdraw the required amount anytime within your approved limit directly to your bank account. - Repay Flexibly:

Repay the used amount in flexible EMIs or repay early to save on interest and reuse your credit limit when needed.

Pros and Cons of Rufilo

| Pros of Rufilo | Cons of Rufilo |

| Instant personal credit line with flexible withdrawals | Approval amount depends on credit score and income stability |

| Fast disbursal and paperless process | Not ideal for users with poor credit history |

| Reusable credit limit withdrawn again after repayment | Limited to smaller loan amounts for new users |

| Reusable credit limit withdraw again after repayment | May charge processing or convenience fees |

| Suitable for both salaried and self-employed individuals | Availability may vary across regions |

| Helps improve credit score through timely repayments | Interest rates can be higher compared to bank loans |

Why Do Cash Advance Apps Work?

When you need emergency funds just before your next payday, you join many others who face this situation. Cash advance apps function as your financial backup to provide access to your earned wages before your next payday arrives.

These apps function as your financial partner to let you access your already earned wages before your next payday arrives. The process requires no visits to banks. The system operates without charging interest on credit cards or requiring loans from predatory lenders. The service provides a simple method to manage your expenses through a fast and clear process.

Here’s Why the magic happens.

Connect Your Paycheck

The first step requires you to connect your bank account or your paycheck information to the application. The cash advance applications Earnin, Dave, and MoneyLion use your financial data to determine your regular earnings and payment schedule.

Request a Cash Advance

The verification process allows you to access a portion of your future paycheck, which ranges from $50 to $500. The apps enable users to increase their borrowing limits through positive payment history.

Instant or Same-Day Transfer

You can obtain immediate access to funds through the application since it provides fast transfer options at affordable rates. The application deposits funds directly into your account within one to two business days after your request. The application provides faster access to funds than traditional payday loan procedures.

Automatic Repayment on Payday

The application will automatically withdraw the borrowed amount from your paycheck at the time of your next payment arrival. The system operates with complete ease because it eliminates the need for manual payment handling and reminder systems. The system operates with complete ease because it eliminates all manual payment requirements.

Optional Tips or Subscription Fees

Instead of charging high interest rates like traditional loans, some apps ask for a small tip or a monthly membership fee. You choose what feels fair; that’s what makes these platforms more user-friendly and transparent.

Payday Loan Apps vs. MoneyLion App: What’s the Better Choice?

The wait for payday becomes endless when you have limited financial resources. People who need immediate financial assistance begin searching for payday loan applications through their mobile devices. The majority of people believe these applications provide instant financial solutions, yet they do not solve long-term money problems.

The fast money provided by payday loan apps leads to excessive interest rates and concealed costs, which create debt problems that people cannot escape. Your first loan becomes a debt burden that forces you to take out additional loans to pay it off, which results in your upcoming paychecks becoming unavailable. The brief financial assistance turns into an extended period of financial distress.

The MoneyLion App provides users with a different financial solution than traditional payday loan apps. The MoneyLion App provides users with complete financial management tools beyond basic loan services. The application functions as your individual financial management system instead of providing a single emergency loan. The platform enables users to obtain interest-free cash advances while they build their credit score and invest their money, and monitor their checking account activities. The platform delivers intelligent financial management instead of providing quick access to funds.

The main distinction between these two options lies in their purpose. Payday loan apps enable users to survive their current situation. MoneyLion enables users to achieve financial success during the following year. The platform exists to support users who want to escape their recurring pattern of living from paycheck to paycheck instead of remaining trapped.

Select the financial solution that provides money access while simultaneously creating a better financial outlook for your future. The actual strength lies in understanding Why to direct your financial resources toward your advantage.

MoneyLion enables users to achieve better financial decisions through its services, which operate without any deceptive practices or hidden costs.

Top 7 Key Features to Look for in a Cash Advance App Like MoneyLion

A trustworthy cash advance application becomes essential when financial resources become limited. Different applications provide different levels of service to their users. The apps that offer quick cash access through their services will charge you additional costs that you need to discover. The apps that focus on your financial health will provide you with better service than those that do not. Before you start downloading cash advance apps, you should understand what features make a trustworthy application, because MoneyLion provides such benefits.

The top applications provide financial management services alongside money growth solutions and protection features. A cash advance application that provides genuine value to users should operate as a financial ally instead of leading users into payday loan debt. The following characteristics distinguish advanced applications from basic ones.

1. Instant Access to Cash (Without the Stress)

The need for immediate financial assistance makes waiting for days completely unacceptable. The best apps provide instant or same-day cash advances through a process that eliminates all paperwork requirements and credit checks. MoneyLion provides users with instant access to their earned money through instant transfer because emergencies require immediate resolution.

2. Zero or Low Fees

The discovery of hidden fees will instantly destroy your sense of relief. A good application should present clear and reasonable costs that avoid both excessive interest rates and hidden processing fees. MoneyLion provides users with interest-free cash advances, and users can choose to add optional tips.

3. No Credit Check Hassles

Your financial history should not determine your current financial situation. The correct application system recognizes that your previous financial mistakes should not affect your current financial situation. The application system should base its decisions on your income level and transaction history instead of your credit score.

4. Smart Budgeting Tools

The ability to manage your money effectively becomes more valuable than quick access to cash. A good application should include built-in budget tracking features together with spending analysis and financial guidance to help users develop improved money management skills. MoneyLion provides users with customized financial analysis that helps them maximize their dollar value.

5. Credit-Building Opportunities

A cash advance app that provides only temporary financial assistance does not offer lasting benefits. An application that enables users to construct their credit standing provides them with enduring financial power. Through MoneyLion, users can enhance their credit rating while obtaining financial assistance that surpasses what typical payday loan applications offer.

6. Safe and Secure Banking

Your financial data requires absolute protection because you are sharing your bank information and paycheck details with the application. Your financial data remains protected through bank-grade encryption and multi-layer authentication when you select an application.

7. All-in-One Financial Ecosystem

A top-notch cash advance application extends its functionality beyond basic advance services. The application provides users with banking services and investment tools, credit monitoring, and savings features within a single platform. MoneyLion stands out because it functions as a financial control center, which enables users to control their money instead of simply borrowing it.

How Much does It Cost to Develop a Cash Advance App?

The Development of a cash advance app requires more than coding because it needs to create an effortless financial system that users can depend on. The final price for building a cash advance application depends on multiple essential elements, which include application complexity, Design standards, technology selection, and feature implementation scope.

The Development expenses for your app will increase when you add sophisticated features, including instant fund transfers, intelligence artificial credit evaluation, and real-time expense monitoring. The Development of user-friendly interfaces with professional UI/UX Design expertise leads to better user engagement but increases project costs.

The Development expenses for creating a cash advance application similar to MoneyLion fall between $15,000 and $35,000 USD. The estimated cost will change according to.

- The feature set (basic vs. advanced functionalities)

- The platform (iOS, Android, or cross-platform)

- The Development team’s experience and location

- The level of security and compliance required

- Integration with banking APIs or third-party payment systems

A professional fintech app Development company should be your first choice when you want to build an application with advanced features, security, and scalability. The team at encodedots will assist you in developing your concept while establishing your technology needs and creating a detailed project cost estimate that matches your business objectives.

Quality app Development expenses serve a dual purpose because they establish user trust and deliver financial benefits and convenience through your application.

Conclusion

The emergence of cash advance applications provides essential financial assistance to people who need emergency funds before their next payday arrives. Users can access fast and protected financial assistance through these apps, which provide better alternatives than conventional loans and excessive interest rates.

The financial management tools provided by MoneyLion and other trusted apps enable users to handle unexpected costs while gaining control over their financial situation. The apps provide users with borrowing capabilities while simultaneously teaching them to manage their finances effectively.

Cash advance apps function as short-term financial solutions instead of establishing permanent financial dependence. The path to financial stability requires you to develop better budgeting skills while monitoring your spending and building savings reserves.

You should develop your own cash advance application if the concept of these apps motivates you. A skilled fintech Development partner can help you create a customized cash advance application that meets contemporary user requirements. The mobile app Development experts at encodedots will lead you through the complete Development journey, starting with concept creation until your app deployment, to achieve market differentiation in financial applications.

The main objective of cash advance apps, whether you use them or create them, remains to simplify financial management while enhancing security and intelligence for all users.